Coupling Groups, Copulas and Variable Reordering

This guide explains how PAL manages dependencies between stochastic variables. It covers three interconnected concepts:

Coupling Groups — automatic tracking of related variables

Copulas — creating dependency structures between variables

Variable Reordering — how copulas work under the hood

A runnable version of all examples below is available at

examples/example_couplings_and_copulas.py.

1. Coupling Groups

What Is a Coupling Group?

Every StochasticScalar in PAL belongs to a coupling group — a

set of variables that are linked by computation. When you create an

independent variable, it gets its own coupling group. When you combine

variables in arithmetic, their coupling groups merge.

from pal import config, distributions, set_random_seed

config.n_sims = 10_000

set_random_seed(42)

motor = distributions.LogNormal(mu=14, sigma=0.5).generate()

prop = distributions.LogNormal(mu=15, sigma=0.8).generate()

# Each starts in its own group

motor.coupled_variable_group is prop.coupled_variable_group

# => False

When variables are combined, they become coupled:

total = motor + prop

# Now all three share the same coupling group

motor.coupled_variable_group is prop.coupled_variable_group

# => True

len(motor.coupled_variable_group)

# => 3

Derived variables also join automatically:

motor_with_expenses = motor * 1.1

motor_with_expenses.coupled_variable_group is motor.coupled_variable_group

# => True

len(motor.coupled_variable_group)

# => 4

Why Coupling Groups Matter

Coupling groups solve a critical problem: when a copula reorders one variable’s simulations, all related variables must be reordered in exactly the same way to preserve their mathematical relationships.

Consider this scenario:

set_random_seed(42)

loss_a = distributions.LogNormal(mu=14, sigma=0.5).generate()

loss_b = distributions.LogNormal(mu=15, sigma=0.8).generate()

# Derive a variable from loss_a

loss_a_expenses = loss_a * 1.15 # 15% expense loading

Before any copula, loss_a and loss_a_expenses have a perfect 1.15×

relationship because simulation i of both variables corresponds to the

same underlying scenario:

loss_a first 5: [1751476. 1113583. 2057538. 1557236. 622980.]

loss_a_expenses first 5: [2014197. 1280620. 2366169. 1790821. 716427.]

Ratio: [1.15 1.15 1.15 1.15 1.15]

Now apply a copula to correlate loss_a with loss_b:

from pal import copulas

copulas.GaussianCopula(

[[1.0, 0.7], [0.7, 1.0]]

).apply([loss_a, loss_b])

After the copula reorders loss_a, the 1.15× ratio is preserved:

Ratio (still 1.15!): [1.15 1.15 1.15 1.15 1.15]

This works because PAL’s coupling group system automatically reordered

loss_a_expenses with the same permutation as loss_a.

Without coupling groups, loss_a_expenses would retain its original

ordering while loss_a was shuffled, breaking the 1.15× relationship

and producing nonsensical results.

2. Copulas

A copula defines a dependency structure (correlation pattern) between random variables. PAL provides several copula families, each producing different patterns of dependence, especially in the tails.

Available Copula Types

Family |

Class |

Key Parameters |

Tail Dependence |

|---|---|---|---|

Elliptical |

|||

Gaussian |

|

Correlation matrix |

None |

Student’s T |

|

Correlation matrix, |

Symmetric |

Archimedean |

|||

Gumbel |

|

|

Upper |

Clayton |

|

|

Lower |

Frank |

|

|

None |

Joe |

|

|

Upper |

Extreme value |

|||

MM1 |

|

|

Upper |

Galambos |

|

|

Upper |

Hüsler-Reiss |

|

|

Upper |

Extremal T |

|

|

Upper |

Other |

|||

Plackett |

|

|

None |

Elliptical copulas (Gaussian, Student’s T) accept a full correlation matrix and naturally support any number of dimensions.

Archimedean copulas (Gumbel, Clayton, Frank, Joe) take a single

theta parameter and the dimension n.

Extreme value copulas (MM1, Galambos, Hüsler-Reiss, Extremal T) model upper tail dependence and are suited for modelling joint extreme events. They have varying parameterisations — see the API docs for details.

Plackett copula is a bivariate copula controlled by a single

parameter delta that can model both positive and negative dependence.

Comparing Copula Types

from pal import config, copulas, distributions, set_random_seed

import numpy as np

config.n_sims = 10_000

Independent (no copula)

set_random_seed(42)

x = distributions.LogNormal(mu=10, sigma=1.0).generate()

y = distributions.LogNormal(mu=10, sigma=1.0).generate()

np.corrcoef(x.ranks.values, y.ranks.values)[0, 1]

# => -0.0034 (approximately zero)

Gaussian Copula

set_random_seed(42)

x = distributions.LogNormal(mu=10, sigma=1.0).generate()

y = distributions.LogNormal(mu=10, sigma=1.0).generate()

copulas.GaussianCopula([[1.0, 0.8], [0.8, 1.0]]).apply([x, y])

np.corrcoef(x.ranks.values, y.ranks.values)[0, 1]

# => 0.7853

Gumbel Copula (upper tail dependence)

set_random_seed(42)

x = distributions.LogNormal(mu=10, sigma=1.0).generate()

y = distributions.LogNormal(mu=10, sigma=1.0).generate()

copulas.GumbelCopula(theta=3.0).apply([x, y])

np.corrcoef(x.ranks.values, y.ranks.values)[0, 1]

# => 0.8465

Variables jointly tend to be large together — important for modelling joint catastrophic losses.

Clayton Copula (lower tail dependence)

set_random_seed(42)

x = distributions.LogNormal(mu=10, sigma=1.0).generate()

y = distributions.LogNormal(mu=10, sigma=1.0).generate()

copulas.ClaytonCopula(theta=4.0).apply([x, y])

np.corrcoef(x.ranks.values, y.ranks.values)[0, 1]

# => 0.8479

Variables jointly tend to be small together — dependence is concentrated in the lower tail.

Student’s T Copula (symmetric tail dependence)

set_random_seed(42)

x = distributions.LogNormal(mu=10, sigma=1.0).generate()

y = distributions.LogNormal(mu=10, sigma=1.0).generate()

copulas.StudentsTCopula(

[[1.0, 0.7], [0.7, 1.0]], dof=3

).apply([x, y])

np.corrcoef(x.ranks.values, y.ranks.values)[0, 1]

# => 0.6658

Like the Gaussian copula but with symmetric tail dependence — extreme values are more likely to co-occur. The lower the degrees of freedom, the stronger the tail dependence.

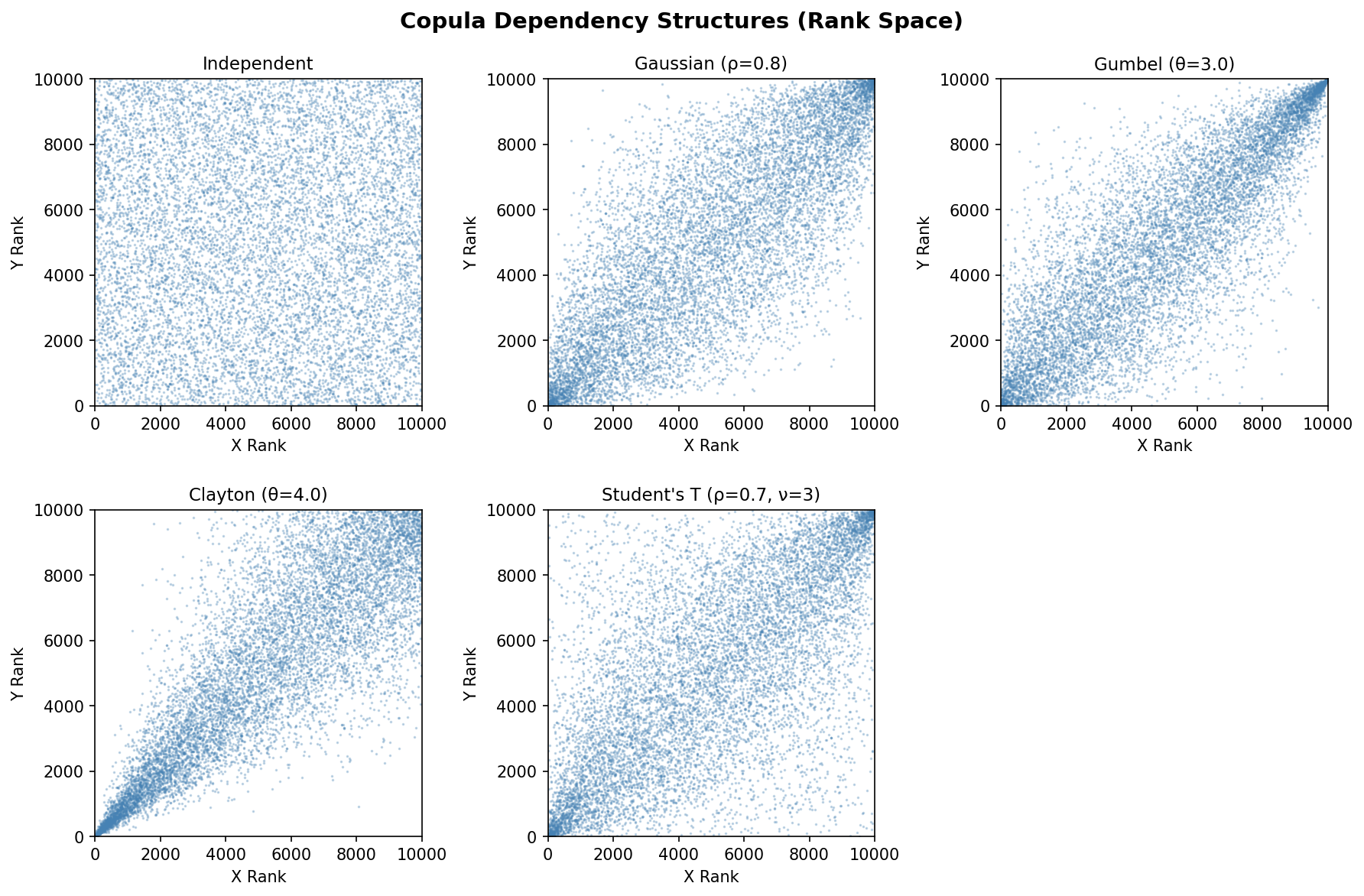

Scatter Plots — Rank Space

The best way to understand how copulas differ is to plot the variables in rank space (plotting the ranks rather than the raw values). This removes the effect of the marginal distributions and isolates the dependency structure.

Independent: uniform scatter with no pattern

Gaussian: elliptical concentration along the diagonal

Gumbel: strong clustering in the upper-right corner (upper tail)

Clayton: strong clustering in the lower-left corner (lower tail)

Student’s T: similar to Gaussian but with heavier concentration in both corners (both tails)

The interactive version of this chart (with plotly) is available in

examples/example_couplings_and_copulas.ipynb.

3. Variable Reordering

How apply() Works

When you call copula.apply([var_x, var_y]), PAL performs these steps:

Generate copula samples: The copula creates correlated uniform random variables with the desired dependency structure.

Compute rank indices: For each copula sample, compute the rank ordering (which simulation should be 1st, 2nd, 3rd, etc.).

Reorder simulations: Rearrange each variable’s simulations so their ranks match the copula’s rank structure.

Preserve marginals: The same set of values is retained — only their ordering changes.

Merge coupling groups: All input variables (and their coupled variables) are merged into a single coupling group.

Seeing Reordering in Action

To make the reordering concrete, here is a small example with only 8 simulations. We can see exactly which values move where:

config.n_sims = 8

set_random_seed(42)

x = distributions.Normal(0, 1).generate()

y = distributions.Normal(0, 1).generate()

Before the copula, X and Y have unrelated orderings:

Sim: 0 1 2 3 4 5 6 7

X values: [ 0.752, -0.154, 1.074, 0.517, -1.315, 1.971, 0.710, 0.793]

Y values: [-1.135, -0.125, -0.330, 1.452, 0.369, 0.926, -0.142, -0.748]

X ranks: [ 4, 1, 6, 2, 0, 7, 3, 5]

Y ranks: [ 0, 4, 2, 7, 5, 6, 3, 1]

Notice that X and Y ranks are unrelated — when X is high (rank 7 in sim 5), Y has rank 6. When X is low (rank 0 in sim 4), Y has rank 5.

copulas.GaussianCopula([[1, 0.9], [0.9, 1]]).apply([x, y])

After the copula, the Y values have been shuffled so their ranks align with X’s ranks:

Sim: 0 1 2 3 4 5 6 7

X values: [ 0.752, -0.154, 1.074, 0.517, -1.315, 1.971, 0.710, 0.793]

Y values: [-0.125, -0.748, 0.926, -0.142, -1.135, 1.452, -0.330, 0.369]

X ranks: [ 4, 1, 6, 2, 0, 7, 3, 5]

Y ranks: [ 4, 1, 6, 3, 0, 7, 2, 5]

Key observations:

X values are unchanged — the same 8 numbers in the same positions

Y values are the same set of numbers, but reordered — e.g. the value

1.452moved from sim 3 to sim 5Ranks now nearly match: when X has rank 7 (sim 5), Y also has rank 7. When X has rank 0 (sim 4), Y also has rank 0

Sorted values are identical before and after:

np.allclose(sorted(x.values), sorted_x) # => TrueRank correlation jumped to 0.9762 (from ~0)

This is the fundamental mechanism: copula application is a permutation, not a transformation.

Marginal Preservation

A critical property of copula application is that marginal distributions are exactly preserved. The same values exist before and after — only their ordering changes:

config.n_sims = 10_000

set_random_seed(42)

var_x = distributions.Normal(0, 1).generate()

var_y = distributions.Normal(0, 1).generate()

sorted_x = np.sort(var_x.values)

sorted_y = np.sort(var_y.values)

copulas.GaussianCopula(

[[1.0, 0.9], [0.9, 1.0]]

).apply([var_x, var_y])

# Marginals are unchanged

np.allclose(np.sort(var_x.values), sorted_x) # => True

np.allclose(np.sort(var_y.values), sorted_y) # => True

# But now correlated

np.corrcoef(var_x.ranks.values, var_y.ranks.values)[0, 1]

# => 0.8903

Reordering Across a Chain of Derived Variables

Coupling groups enable transitive reordering across chains of derived variables:

set_random_seed(42)

base_loss = distributions.LogNormal(mu=14, sigma=0.5).generate()

gross_loss = base_loss * 1.0

expense_loaded = gross_loss * 1.10

tax = expense_loaded * 0.21

net_loss = expense_loaded - tax

# All 5 variables share one coupling group

len(base_loss.coupled_variable_group)

# => 5

When a copula is applied to base_loss and an independent variable,

every variable in the chain is reordered together:

cat_loss = distributions.LogNormal(mu=16, sigma=1.2).generate()

copulas.GumbelCopula(theta=1.5).apply(

[base_loss, cat_loss]

)

# All ratios are preserved

gross_loss.values[:3] / base_loss.values[:3]

# => [1. 1. 1.]

expense_loaded.values[:3] / gross_loss.values[:3]

# => [1.1 1.1 1.1]

tax.values[:3] / expense_loaded.values[:3]

# => [0.21 0.21 0.21]

4. Multivariate Copulas

Elliptical copulas naturally extend to any number of dimensions. Here is an example correlating 4 lines of business:

set_random_seed(42)

lobs = {

"Motor": distributions.LogNormal(mu=14, sigma=0.4).generate(),

"Property": distributions.LogNormal(mu=15, sigma=0.6).generate(),

"Liability": distributions.LogNormal(mu=13, sigma=0.5).generate(),

"Marine": distributions.LogNormal(mu=12, sigma=0.7).generate(),

}

corr_matrix = [

[1.0, 0.6, 0.3, 0.2],

[0.6, 1.0, 0.4, 0.3],

[0.3, 0.4, 1.0, 0.5],

[0.2, 0.3, 0.5, 1.0],

]

copulas.GaussianCopula(corr_matrix).apply(list(lobs.values()))

The resulting rank correlations closely match the input:

Motor Property Liability Marine

Motor 1.000 0.578 0.264 0.177

Property 0.578 1.000 0.361 0.261

Liability 0.264 0.361 1.000 0.479

Marine 0.177 0.261 0.479 1.000

Compare with input: [0.6, 0.3, 0.2], [0.4, 0.3], [0.5] — the rank

correlations are close but not exact due to finite sample size

(10,000 simulations).

To be completely precise, we should compare the rank correlation to the Spearman’s :math:\rho_S of the Gaussian copula, which is related to the underlying correlation parameter :math:r by:

.. math::

\rho_S = \frac{6}{\pi}\asin\left(\frac{r}{2}\right)

5. generate() vs apply()

Copulas have two main methods:

generate() — Create New Samples

Returns correlated uniform [0, 1] samples. Use this when you want

raw copula samples to feed into inverse CDF transforms manually:

samples = copulas.GaussianCopula(

[[1.0, 0.8], [0.8, 1.0]]

).generate()

samples[0].mean() # => ~0.5 (uniform)

samples[1].mean() # => ~0.5 (uniform)

apply() — Reorder Existing Variables

Reorders existing StochasticScalar variables to match the copula’s

dependency structure. This is the most common workflow:

v1 = distributions.Gamma(alpha=5, theta=1000).generate()

v2 = distributions.Pareto(shape=2, scale=10000).generate()

copulas.GaussianCopula(

[[1.0, 0.8], [0.8, 1.0]]

).apply([v1, v2])

# Means unchanged - only the ordering changed

# Rank correlation: 0.7867

Key difference: generate() creates new data; apply() restructures

existing data. In most actuarial models, you’ll use apply() because

you’ve already generated variables from their marginal distributions and

want to impose a dependency structure.

6. Frequency-Severity Models with Copulas

In actuarial modelling, losses are often represented as compound

distributions using FrequencySeverityModel. After generating

event-level simulations, you aggregate them to get simulation-level

totals, then use copulas to impose dependencies between lines of

business.

Two Lines of Business

from pal.frequency_severity import FrequencySeverityModel

config.n_sims = 10_000

set_random_seed(42)

# Motor: 50 claims/year, LogNormal severity

motor_model = FrequencySeverityModel(

freq_dist=distributions.Poisson(mean=50),

sev_dist=distributions.LogNormal(mu=10, sigma=1.5),

)

motor_events = motor_model.generate()

# Property: 20 claims/year, Pareto severity

property_model = FrequencySeverityModel(

freq_dist=distributions.Poisson(mean=20),

sev_dist=distributions.Pareto(shape=2.5, scale=50_000),

)

property_events = property_model.generate()

# Aggregate to simulation-level totals

motor_agg = motor_events.aggregate()

property_agg = property_events.aggregate()

Before the copula, the two lines are independent:

Before copula:

Motor aggregate mean: 3,373,050

Property aggregate mean: 1,664,453

Rank correlation: -0.0069

Now apply a Gaussian copula with ρ=0.6 (both lines worsen in the same economic environment):

copulas.GaussianCopula(

[[1, 0.6], [0.6, 1]]

).apply([motor_agg, property_agg])

After the copula, losses are correlated but marginals are preserved:

After Gaussian copula (rho=0.6):

Motor aggregate mean: 3,373,050

Property aggregate mean: 1,664,453

Rank correlation: 0.5780

Combined portfolio:

Mean: 5,037,503

Std: 1,744,284

99.5th percentile: 12,192,519

The means are identical before and after — only the joint behaviour changed. The 99.5th percentile of the combined portfolio reflects the positive dependence: bad years for motor tend to also be bad years for property.

Coupling with Catastrophe Losses

You can also use copulas to link frequency-severity aggregate losses

with standalone catastrophe variables. Because aggregate() and

occurrence() return StochasticScalar objects that share a coupling

group with the underlying events, reordering the aggregate

automatically reorders the max-event loss too:

set_random_seed(42)

model = FrequencySeverityModel(

freq_dist=distributions.Poisson(mean=30),

sev_dist=distributions.LogNormal(mu=10, sigma=1.5),

)

events = model.generate()

agg_loss = events.aggregate() # total loss per sim

max_loss = events.occurrence() # largest single event per sim

cat_loss = distributions.LogNormal(mu=16, sigma=1.2).generate()

copulas.GumbelCopula(theta=2.0).apply(

[agg_loss, cat_loss]

)

The Gumbel copula introduces upper tail dependence — years with high attritional losses also tend to have high catastrophe losses:

After Gumbel copula (theta=2.0):

Agg loss mean: 2,022,548

Max event mean: 637,503

Cat loss mean: 18,398,184

Rank corr (agg-cat): 0.6874

Rank corr (max-cat): 0.5818

Note that the max-event loss is also correlated with the catastrophe

loss (rank corr 0.58) even though the copula was only applied to the

aggregate. This is because aggregate() and occurrence() share a

coupling group with the underlying FreqSevSims events.

Important Constraints

Variables must be independent before

apply(): You cannot apply a copula to variables that are already coupled (i.e., in the same coupling group). PAL raises aValueErrorif you try.Coupling is permanent: Once variables are coupled (either through arithmetic or copula application), they remain in the same coupling group for the rest of the simulation.

Order matters: The order of variables in the list passed to

apply()must match the order of dimensions in the copula’s correlation matrix.

References

Nelsen, R. B. (2006). An Introduction to Copulas, 2nd ed. Springer. — The standard textbook on copula theory; covers all major families, properties, and constructions.

McNeil, A. J., Frey, R. & Embrechts, P. (2015). Quantitative Risk Management: Concepts, Techniques and Tools, 2nd ed. Princeton University Press. — Chapters 7–8 give an accessible treatment of copulas in a risk-management context.

Iman, R. L. & Conover, W. J. (1982). “A distribution-free approach to inducing rank correlation among input variables.” Communications in Statistics — Simulation and Computation, 11(3), 311–334. — The original rank-reordering algorithm used by PAL’s

apply()method.Joe, H. (2014). Dependence Modeling with Copulas. CRC Press. — Comprehensive reference covering Archimedean, elliptical, and extreme-value copula families.

Embrechts, P., Lindskog, F. & McNeil, A. (2003). “Modelling dependence with copulas and applications to risk management.” In Handbook of Heavy Tailed Distributions in Finance, Elsevier. — Practical guide to choosing and calibrating copulas for insurance and finance applications.